On Monday last week, the White House made much ado of an announcement that it had secured commitments from a collection of large Internet Service Providers (ISPs) to adjust speed tiers and monthly costs for their existing plans so as to be able to offer a $30/month, minimum 100 megabit per second (Mbps) download offering for low-income households across the country. The goal was to create plans for households that qualify for the $14.2 billion Affordable Connectivity Program (ACP) to get access to faster connections while ensuring no additional out-of-pocket costs. The recent White House announcement said that the 20 private-sector providers that have joined together cover 80 percent of households (skewed towards urban areas).

There’s no argument that the move will directly benefit hundreds of thousands of households by boosting their wireline connections and reducing their monthly expenses. And yet, it’s a treatment of the symptom rather than the disease, as the administration continues to refuse to address the larger structural dynamics that have made Internet access increasingly expensive in this country and perpetuated a broken marketplace via poor regulation and a lack of strong leadership.

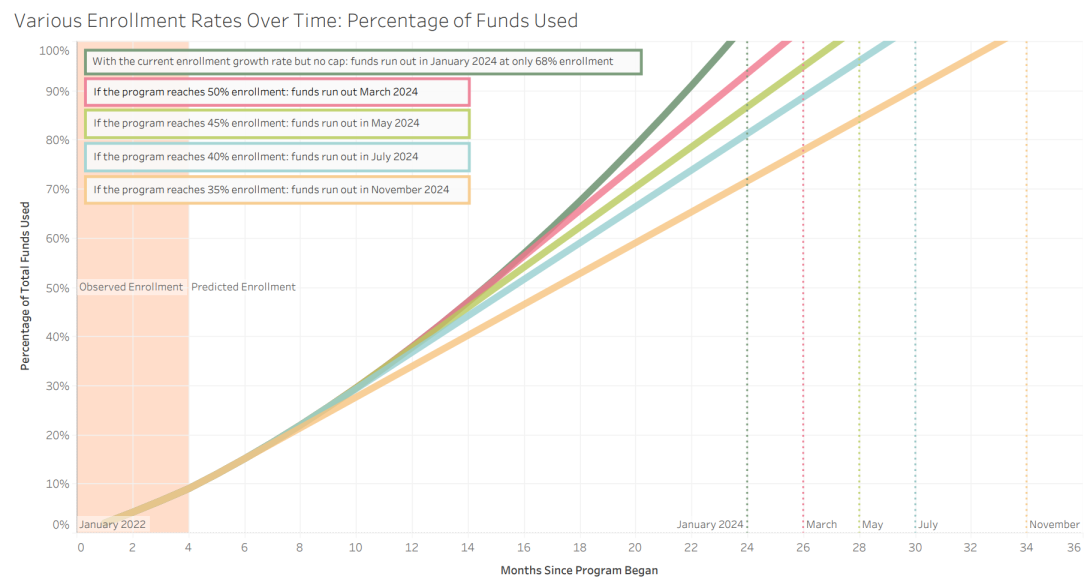

This will become immediately apparent the moment that the Affordable Connectivity Program runs out of money, and those households suddenly face higher costs with no option for recourse. Our analysis shows that even if only a third of eligible households ultimately enroll (ten percent more households than are enrolled today), absent an additional allocation, the fund will be exhausted by the beginning of November 2024. But even under the best-case scenario, with the benefit reaching as many people as possible, current enrollment rates show that only 68 percent of eligible households will be able to sign up before the funds run out. In this model, the money will be exhausted just 18 months from now, on January 1st, 2024.

A Necessary Benefit, But There Are Enrollment Disparities

Today, 11.8 million households are enrolled out of an eligible 48 million households in the Affordable Connectivity Program, which means that as a nationwide average, a little less than 25 percent of those that qualify for the benefit are using it.

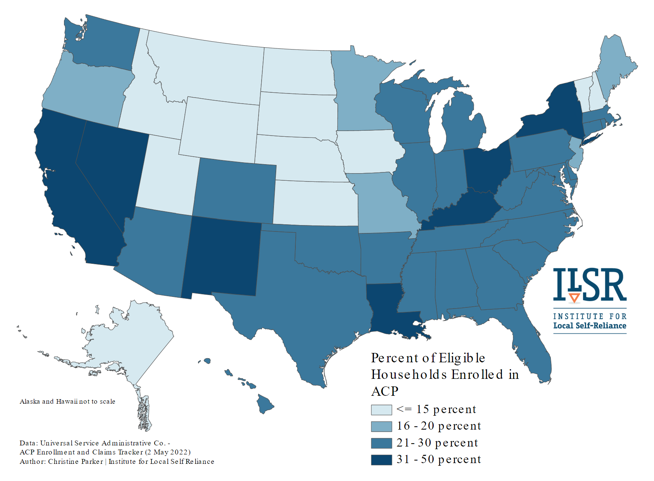

The reality on the ground is that enrollment efforts in some states are going much better than others. No state has yet broken through 50 percent enrollment of eligible households, but California, Nevada, New Mexico, Louisiana, Kentucky, Ohio, and New York all lead the pack with more than 30 percent of eligible households enrolled. Those states struggling to see eligible households signed up for the benefit - with less than fifteen percent enrolled - are clustered almost exclusively in the upper plains, with the additions of New Hampshire and Vermont. Eleven states fall into this category. The rest fall somewhere in the middle. See the map below for more; darker shades of blue represent higher enrollment rates. See a larger version of the map here.

When Will the Funds Run Out?

Many factors play into how many of the 48 million eligible households will ultimately sign up for the benefit. Direct outreach efforts likely have the biggest impact. There are others, though too, including everything from overcoming distrust of programs which seem to offer something for free, to how good of a job (or not, in many instances) Internet Service Providers do in advertising their involvement in the program and walking subscribers through the process of setting up. For more on the obstacles the program faces in rural and urban areas, read USC-Annenberg Associate Professor of Communication Hernan Galperin’s analysis of the precursor Emergency Broadband Benefit (EBB) program (which functions much the same).

But as states, nonprofits, ISPs, and localities continue to work through these challenges, the reality is that the ACP bank account is being drawn down nearly $350 million each month, and ever faster as more sign up. We wanted to get a sense of how quickly it would reach zero, and how that would be affected by how many people will ultimately sign up.

To conduct this analysis, we used data from the American Community Survey to determine the number of eligible households per state, and then calculated the percent of households enrolled of those that are eligible. We were also interested in when the funds for ACP would be depleted according to various national enrollment rates. Today the fund is at 25 percent enrollment. We made several predictions based on scenarios ranging from 35 percent enrollment to no cap on enrollment.

The nationwide enrollment data for the Emergency Broadband Benefit and the Affordable Connectivity Program (combined through April 25, 2022) were used as the response variable in a linear regression model with a 95% confidence level. Read more on how we calculated the number of households eligible and created the predictions here.

See the graph below for when the ACP funds will be depleted at different enrollment rates. See a larger version of the graph here.

Different enrollment caps are graphed along the x-axis on the image above, along with a dotted line to signify the month and year the fund will be exhausted. The y-axis shows how much of the fund has been spent as time goes on.

It’s hard to know how many of the eligible households will sign up for the ACP. Some experts think the rate will increase as the program continues. Today it’s at 25 percent. Comparing it to the existing $9.25/month Lifeline benefit isn’t particularly helpful; the ACP benefit is three times larger, and enrollment rates in Lifeline have always been frustratingly low despite the fact that the program is nearly 40 years old.

However, assuming the current enrollment growth rate continues, with no artificial cap placed on the households that will take advantage of the program, we project that the Affordable Connectivity Program will be depleted just before January 2024, maxing out at 68 percent of eligible households enrolling. On the other end of the spectrum, if the program reaches just 35 percent enrollment under the current enrollment growth rate, the funds will run out by November of 2024. Likely, it will land somewhere in between.

If program enrollment stops at 40 percent under the current enrollment growth rate, the funds will run out by July of 2024. If program enrollment stops at 45 percent under the current enrollment growth rate, the funds will run out by May of 2024. If program enrollment stops at 50 percent under the current enrollment growth rate, the funds will run out by March of 2024.

Importantly, if state and local efforts improve their outreach efforts and signup efficacy, the total number of households that sign up for the benefit may get higher than 68 percent, but the funds will be depleted sooner than January 2024.

What Happens When It Hits Zero?

In all of these cases, unless Congress reappropriates funds to fill the benefit bank account back up, those families will see their monthly bills jump by $30. To continue to fund the ACP, we’re looking at a permanent commitment of billions to tens of billions of dollars every year - and to be clear, these are public tax dollars, of which the vast majority are disappearing into the pockets of monopoly ISPs that have been posting huge profits in captured markets that they’ve defended against the specter of competition at both at the local and national level for years. It’s also important to remember that under all of these models, assuming no Congressional reappropriation comes, those households that sign up last will only see the benefit for a month or two before being cut off.

One final note regarding the ACP: we’ve seen many publicly owned networks step up and offer free or extremely reduced-cost plans from the start of the pandemic. Longmont, Colorado’s municipal network offers 100 Mbps symmetrical service to income-qualifying households for free. In Hillsboro, Oregon, the municipal network’s BRIDGE program brings symmetrical gigabit connections for $10/month. Many of these predate the ACP, and are demontrative of what can happen with locally owned and controlled network infrastructure operates according to a fundamentally different set of motivations.

*A note on methods: In calculating the life of the fund, we took the lower $30/month household subsidy to project growth, ignoring the larger $75/month Tribal household subsidy (of which there are 164,000 enrolled today). The other uncertainty in this model is that the $100 device benefit also comes out of the same fund. Unfortunately, while USAC does track to some extent the payouts for the device benefit at the zip code level, there are no complete data to use in modeling that impact on the drawdown of the fund. Together, however, both of these mean a drawdown of the fund more quickly than we project, if anything.

Thanks to Associate Researcher Emma Gautier and GIS and Data Visualization and GIS Specialist Christine Parker for the growth models and data analysis, tables, and graphs. This piece could not have happened without them.

{kind=link}

{kind=link}